The Skinny:

Only buy deals that look great in a base case, reasonable in a downside case, and fantastic in an upside case.

My Lightbulb Moment:

Every investor needs to have an investment philosophy. Whether it is in real estate, stocks, private equity, or venture capital, all successful investors stick to a well-defined and dedicated strategy. This allows them to not only set themselves apart, but also allows them to be disciplined and dispassionate in the long-term through the inevitable ups and downs of the economic cycle. If you do not have a strategy, I do not believe you can call yourself an investor.

All investing legends, past and present, had a dedicated approach. Warren Buffett is known for being a disciple of the late Benjamin Graham, who emphasized buying stocks at a big discount to intrinsic value to ensure a margin of safety. Peter Lynch and Philip Fisher emphasized growth more than value when picking stocks and believed in identifying clear catalysts before the crowd. My personal favorite equities investor, John Neff, focused on businesses with strong distributions to avoid relying solely on capital appreciation. In real estate, Sam Zell was known for capitalizing on downturns and on others’ mistakes and was nicknamed the “Grave Dancer” for his ability to find success when things looked gloomy. William Zeckendorf was known for making seemingly outrageous debt-fueled gambles on one-of-a-kind visions and simply betting that demand would follow. It might not be the most prudent, but it was still a strategy.

Throughout my life, I had been knowingly and unknowingly crafting my own investment philosophy. I knew I was more risk-averse than most, but I also firmly believed that this shouldn’t preclude achieving strong returns. I adored the idea of a margin of safety but also believed that growth catalysts are a necessity in any investment. It was a nebulous philosophy for a long time because I could never quite distill it. That is until a lightbulb went off one unsuspecting day. My lightbulb moment came when I was preparing for my annual draft for fantasy football. You see, I suck at fantasy football (I am a hockey guy) and I was always near the bottom, but this time I wanted to try and do better. I read many draft reports online and noticed two phrases that kept coming up again and again. One was “high floor”, which was used to describe players who may not be dazzling stars but will always put up decent points (for me, this was Keenan Allen). The other was “high ceiling” which was used to describe players who might have monster games at the risk of some dismal games with a “low floor” (for me, this was Will Fuller V who unfortunately burned this concept into my mind with his performances that year). Suddenly, it was crystal clear to me, I want both! I want a player with a high floor AND a high ceiling. In fantasy football land, these options are limited because there are only a handful of players who provide this consistently, and they need to be split among your fellow competitors / pals in the league. However, I immediately appreciated the fact that in the real estate world, there are A LOT more candidates that can be “high floor, high ceiling” and that has been my investment philosophy ever since.

High Floor, High Ceiling in Real Estate Investing:

The high floor, high ceiling philosophy is well-known in the investment community, although I proudly think I might be the first to utilize fantasy terms to describe it. In most investment circles, the term that is used more often is something a little stuffier sounding like “asymmetric investment” that describes an opportunity with great upside and limited downside risk. It is music to the ears of any investor, as there are few things better than knowing your money is safe but has the potential to grow substantially.

In stock investing, asymmetry is table stakes for value investors. They only buy deals where there is a very low probability of principal loss and high probability of meaningful upside. However, in real estate, I firmly believe the high floor, high ceiling concept is much more special. Why? Because as a real estate owner / operator, you can directly influence the investment characteristics and create the investment’s asymmetry yourself.

If you find a stock that you feel is very undervalued, that is great! However, you do not really have the power to do anything about it. You basically have to wait around and hope that the company liquidates (the purest way to achieve full value!) or that the rest of the market catches on and bids up the price to a value that you would feel comfortable taking your profits. This could take an indeterminable amount of time. It could take years and you might be missing out on other opportunities that would have reaped more value faster. Remember, time does matter in investing. Being too early can sometimes mean the same thing as being wrong. Buying a deal for $10 and selling it for $15 in 1 year is a better return than buying a deal for $10 and selling it for $30 in 3 years due to the power of time and compounding.

In real estate however, you can make things happen from day 1. As discussed below, you can ensure that a deal has a favorable risk / return profile simply through your own vision and creativity. Through judicious purchasing and a well-executed business plan, tremendous value can be unlocked through your own hand. That power simply does not exist in the stock market.

Another key difference is that real estate will always be inefficient in terms of information. Supercomputers are sifting through stock information in milliseconds, buying and selling automatically to exploit the smallest pricing differences. In the glory days of value investing, a fund manager was able to spot pricing differences through their own hard work in finding more information about a company than others. That is just so hard to do now in the digital age. Everyone can find information about any traded security with a few clicks. Therefore, it is harder to stand out. This will never be a threat in real estate. It is far too fragmented and heterogeneous.

High Floor:

Warren Buffett famously said “the first rule of an investment is don’t lose money. And the second rule of an investment is don’t forget the first rule”. This very much holds true for real estate as well, except I would make it even more stringent and say that the first rule is to always generate a reasonable rate of return, aka a high floor.

One of the first questions you should ask yourself when reviewing an opportunity is “how badly can this deal go and how easily can I prevent that from happening?” A prerequisite for any asymmetric investment is that it needs to be hard to mess up. The deal must be strong and dynamic enough that even if you miss on some of your projections or execution, you can still provide a good outcome to your investors. After all, no one can predict the future and every single valuation is imperfect because of that immutable fact. Things happen in the world that are unknowable. Your fancy NPV calculator is only a step or two removed from a fortune cookie. Therefore, the best way to ensure a high floor is to focus on the things you can control.

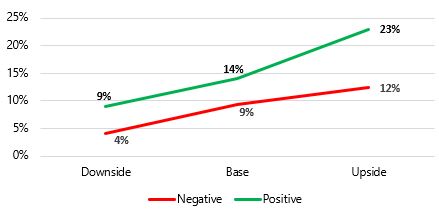

The first thing that you can control is the price you pay for a deal. Don’t overpay. Plain and simple. There is nothing worse than immediately putting yourself in a situation where everything needs to go right to succeed, because they rarely do. No one should want to go into a game knowing that they are either going to lose or tie. Yet that is exactly what some groups do and I see this all the time in major markets. A nice building that is really worth $100mm gets bid up by multiple buyers to $110mm+ because they “believe” that outsized rent growth or something will justify their number in 5 years. Ok, that might end up being true, but do you really want to let general market trends that are out of your control dictate the fate of your call? Of course not. When you are reviewing a deal, finalize your base case with some very reasonable (moderately conservative) assumptions. Then run some scenarios to see how much leeway you have in adverse situations, and set your max bid based on the results. Your max bid must look great in a “base” case and decent in a “downside” case, otherwise move on. If a deal only looks good in a base case, then that is an immediate sign that the price and/or risk level is too high. A quick heuristic you can utilize is that a downside case should return 70% of your base case return. If you are looking for a 15% IRR in a base case, the downside should show ~10.5%. If you are looking for 12% in a base case, your downside should show an ~8.5%. You might need to sift through 50+ deals to find one that fits the bill, but as always patience is a virtue, and the payoffs are literally worth it.

The second thing you can control to ensure a high floor is your business plan and execution. One of the most exciting parts of real estate is that you are in control of your fate as the owner and manager. Your business plan is how you can create your own high floor. The most straightforward example is with value-add renovation opportunities. If you find an existing building that is run down and neglected but you realize that with some vision and handywork, it can be a gorgeous asset with much higher rents, you are creating your own high floor. Why? Because through your own hard work, you are literally creating new cash flows and improving a property’s desirability in a market. Let’s say the building has 100 units with rents of $1,000 / unit, but you are confident you can spend $20k / door and get untrended rents of $1,500 / unit, you do not even need to look at market rent growth projections because you are getting a 30% return on your capital through the project, everything else is just gravy. If you miss and only hit $1,250 in rents, a 15% return is still solid and you have still created $300k in new revenues. This is the purest definition of a high floor, making a deal better without relying on any external factors.

Your floor can be further raised by whatever “special sauce” you bring to the table in your business plan (every operator should have at least one special sauce, but the best have several!) whether it is excellent operations, thoughtful amenities, fun resident events, or even something simple like a personal touch and great customer service. You can find countless ways throughout the investment period to add value to your property through creativity and inspiration that do not require a lot of investment. It might be corny, but it is true. This is not a “set and forget” business. Personally, this is why I never invest in “core” deals. There is nothing you can do to create your own high floor. The properties are often brand new and managed by a professional company, so you are at the whim of the broader market. Even a minor downside case could push the returns into the low single digits. I highly recommend focusing on deals where there is “something to do” so you can have a direct impact and shift the risk / return profile heavily into your favor.

Oftentimes these two objectives work together and can be circular. For example, if your special sauce is that you can renovate faster and cheaper than anyone else, you could technically pay more, and your max bid would be higher than others. However, it is critical that you stay disciplined and not exhaust these “levers” during the buying process. Whenever possible, underwrite as conservatively as you can to win the deal, and then outperform in the execution. Under-promising and over-delivering are words to live by.

High Ceiling:

Once you have established that your deal has a high floor and will provide a reasonable rate of return even in a downside case, you can move on to the fun part, which is finding ways to create a high ceiling (raise the roof!) for the investment with an upside case. A high ceiling means there are realistic (not aspirational) paths to providing a much higher return than indicated by your base case. To mirror the heuristic in the high floor section, a high ceiling case would return at least 30% more than the base case. For a 15% IRR base case, you would want ~20% in an upside case or ~15% for a 12% IRR base case. As hinted at earlier, this almost always means identifying and capitalizing on some sort of catalyst either at the market or property level.

A simple example of a market level catalyst would be buying and renovating a property several years in advance of a planned transportation extension such as a light rail or bus terminal. You are already establishing a high floor by buying at a judicious price in what is likely a cheaper up-and-coming area, and by renovating the units to create brand new cash flows for yourself. Even if nothing else happens, you will be happy because you will own a renovated asset that is earning strong annual yields on its own merit, without having to rely on any outside force. You will therefore have underwritten conservative rent growth in your base case with no catalysts. However, if say in Year 4 of your holding period the construction of the light rail is now underway, your rents and value will jump substantially. This is because connected transport systems bring everything in a region “closer” together, narrowing the perceived value gap between close-in and further out submarkets. You can capitalize in a big way either by holding or selling depending on your own objectives and the economic climate. Searching for probable catalysts throughout a market can be a highly lucrative strategy. Even just buying two towns over from a hot one could work via “overflow” effects. It is important however that such catalysts should not be “guaranteed” because then sellers and their brokers will want a much higher value to reflect the future benefits. In the light rail example, you would buy your property right after the initial plan gets a warm reception from the government and citizens, not when the train track is halfway completed.

Catalysts can often be found at the property level as well. A common example of this is through re-zoning. There are some people who spend all day every day buying near worthless pieces of dirt and putting in the sweat and headaches to get them zoned to something more desirable. A developer would pay a big multiple higher for a piece of land that is already zoned because a large part of the risk has already been mitigated and saves them many long hours and headaches. Similarly, I have seen situations where folks will buy a “fractured condo” deal, where they buy a chunk of the condo units but not all of them (say 45 out of 50). They establish their base case and high floor through standard upgrades but pursue an upside case by attempting to acquire the rest of the units and then converting the building to true multifamily. Multifamily goes for much better pricing than condos. In such a case though, you better hope the 5 non-owned units do not find out about the ultimate game plan, otherwise they will hold out for absurd prices!

For office purchases, I have found that catalysts can often be found with a suboptimal rent roll / lease expiration schedule. If you have a large chunk of tenants expiring within the first 1-2 years, it becomes a very intimidating situation for investors (and lenders), often depleting the potential buyer pool. But what if you are in tune with the market and the local leasing teams and know that there are many companies looking for space like the one at the asset? You would have confidence that you could fill the building in short order if current tenants vacate. In this situation, you would try and buy the property at a price that (i) reflects 50% of the tenants (or whatever the market turnover rate is) vacating in a base case and (ii) provides a reasonable rate of return even if all tenants vacate in a downside case. This establishes the high floor for the deal. However, you would work tirelessly after closing to meet with the tenants, understand their intentions, and plan accordingly to renew or replace them before their expirations. If you get the building fully renewed or re-leased, you can really “crush it” with a big exit value. Yet all you really did was put in the work that others did not want to do, mitigated your biggest risks, and ensured a good outcome in any situation.

When it comes to market vs property level catalysts, I highly prefer the latter. Again, one of the most beautiful things about real estate is the ability to control your fate and have a direct impact. While market catalysts can be great because you do not have to do anything but wait, this is a passive approach and successful real estate investors are not passive. At the property level, you can constantly brainstorm ideas to boost rents and values to outperform your base case. If you can create multiple property level catalysts with some probable market level catalysts, then you have the perfect path to a very high ceiling.

Summary:

A high floor, high ceiling mentality is the only way to look at real estate investing in my opinion. Keeping those two objectives at the top of your mind will ensure that you do not fall prey to dangerous optimism like so many other investors. Protect your downside through judicious buying and clever business plans, while broadening your upside by identifying a range of catalysts that would allow you to outperform.