The Skinny:

Debt financing is a cornerstone of successful real estate investing and there is nearly always a willing lender out there no matter who you are or what your project is, but you must understand all of your options so you pick the best lender and terms for your specific business plan.

Introduction:

As I tried to hammer home in my debt is good post, financing is a key reason why real estate investing is such a powerful tool for wealth creation. Real estate, especially the housing sector, is generally viewed as safe due to its stability and tangibility, and as such there is a whole universe of lenders who are eager to provide financing to a range of investments.

Since America is such an entrepreneurial place with excellent capital flows, I would also argue that you can get financing for pretty much any project. For a good project, you get to make lenders compete with each other to try and win you over with the best terms. For a bad project, you may have to turn to some less scrupulous lenders who will offer you what you need, but at terms that will likely be atrocious.

This post will give a fairly succinct overview of each major lender food group so that you know what is out there and what the key benefits and drawbacks are for each. This way you can have a solid grasp of which lender would be best for you as soon as you review a deal, which in turn will allow you to underwrite debt terms more accurately. I could write a whole post about each lender based on their requirements and criteria but for this summary post I will keep it much more general.

While I definitely believe you should be very fluent in debt capital markets yourself, I would highly recommend developing a close relationship with some talented mortgage brokers as well. They do financings all day, every day and will be the best resource for you in this world. They will review your deal, ask important questions, point out the strengths and weaknesses, and then ultimately tell you what lender and structure is best to accomplish your goals. In my experience, these guys and gals are usually sharper and more laid back than other brokers since there are heavier technical aspects as well as more consistent dealflow. This means that if you are a strong mortgage broker, you should always be making money, which means less stress and a better attitude towards current and potential clients.

There is no scientific order here but generally they are listed in order of most common / favorable to least common / unfavorable.

Debt Provider #1 – The “Agencies”:

Whether they actually know what they are or they have just heard the names in passing, I think most people know the names Fannie Mae and Freddie Mac. Although I was still a young angsty lad listening to blink-182 in my bedroom during the GFC, I did hear that these groups gained a lot of recognition during that time!

So what are they exactly? Well, whenever you hear the term “agency” in the context of real estate lending, immediately you should think “government involvement”. This is because these are government backed programs (the proper term is “government sponsored entity” or GSE) and they exist purely to facilitate liquidity in the real estate markets. In this context, liquidity refers to a high level of credit availability and strong flows of capital.

The first thing I would note for the agencies is that they are not lenders. All they do is buy loans from actual lenders who are the ones who source and originate the loans. The agencies then bundle these loans and re-sell them as mortgage-backed securities (MBS) to investors such pension funds and insurance firms. Basically, as long as a deal meets the preset requirements of Fannie Mae or Freddie Mac, they will buy the loan from the lender for a small premium. This gives the lender the ability to go make more loans (increasing liquidity / credit) and so on and so forth. This is the virtuous cycle that the U.S. government intentionally tries to perpetuate.

Think of the lender as a baker who makes donuts every single morning, and think of the agencies as a daily customer who will reliably buy every kind of chocolate, strawberry, and vanilla donut that they make. However, the agency customer does not want anything funky like kiwi-strawberry glaze or maple bacon. Nope, they want basic known commodities because they are going to package and resell these donuts to their own customer base, and that customer base never buys anything exotic.

So there are essentially three steps in every agency loan. The first stage is when a lender originates the loan for a borrower (the “primary” market) whose project meets the standards of the agencies. The second stage is when the agencies buy these loans from the original lenders, thereby transferring the loans from the primary market and preparing them for the “secondary” market. The third and final stage is when the agencies bundle a series of these loans and securitize them into an MBS so that it can be traded freely on the secondary market.

One of the most defining features of these entities is that the loans are explicitly (or perhaps implicitly) guaranteed by the full faith and credit of the United States government. In other words, if the borrower messes up badly, these entities will make sure the interest and principal gets paid to the lender / bond investors. In fact, the agencies are the literal intermediary between the borrower’s loan payments and the bond investor distributions. This mechanism makes MBS’ highly desirable since there is much minimal credit risk (these are de facto “AAA” rated bonds). Since there is minimal credit risk, there is a lot of demand from investors. Since there is a lot of demand from investors, the interest rates are low. Since the interest rates are low, agency financing is very popular with real estate investors. If this system is working functionally, everyone is quite happy.

Let’s run through two of the heavy hitters in the agency world, Fannie Mae and Freddie Mac:

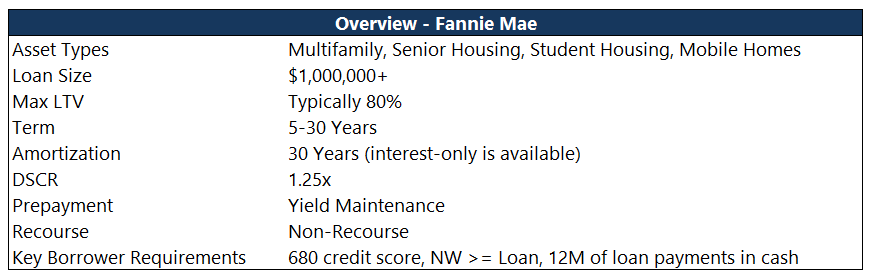

Fannie Mae – full name “Federal National Mortgage Association” aka “FNMA” aka “Fannie Mae”. This program traces its roots to the depression-era New Deal that aided in the recovery of the devastated housing market. Just like today, the goal in 1938 was to create liquidity by leading a secondary mortgage market, which as previously explained, allows primary lenders to make more and more loans. Despite some pretty egregious mishaps during the GFC (TLDR it almost imploded because of bad loans and needed to be taken over by the government), Fannie Mae has been generally successful over its 85+ year existence and its mission remains the same today.

Fannie Mae is often the first stop for multifamily investors because they have some of the lowest rates and best terms available.

PROS:

(+) Excellent interest rates

(+) Longer loan terms

(+) Non-Recourse

(+) High LTV / Proceeds

(+) Widespread availability (via authorized lenders in the DUS network)

CONS:

(-) Stringent eligibility criteria for property type and characteristics

(-) Poor prepayment flexibility (yield maintenance can be brutal)

(-) Time-consuming application process (could take months)

(-) Fairly strict borrower requirements

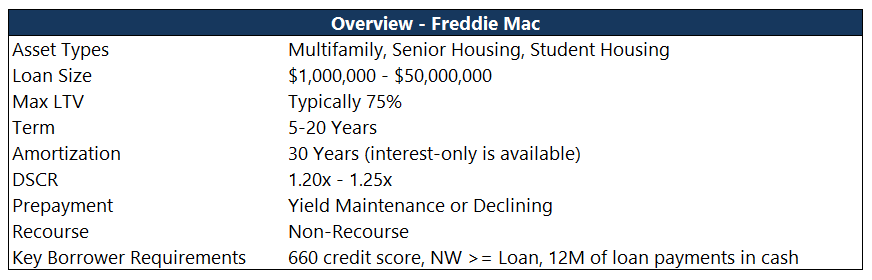

Freddie Mac – full name “Federal Home Loan Mortgage Corporation” aka “FHLMC” aka “Freddie Mac”. This is Fannie Mae’s much younger brother that has many similarities but also some key differences from its sibling. Created in 1970, it was intended to compete with Fannie Mae (sibling rivalry can be a good thing) and to further grow the secondary mortgage market in order to boost liquidity through the same mechanisms as its sister. Some of the key differences include the underwriting criteria, geographic and property preferences, and who each sibling buys the loans from. Fun fact about Freddie Mac is that it gets a shoutout in a famous country song called “Red Solo Cup”.

As intended, the two compete with each other and when you explore financing for multifamily, you will almost certainly explore both options. See if you can spot the differences between the two.

PROS:

(+) Excellent interest rates

(+) Longer loan terms (though not as long as Fannie)

(+) Non-Recourse

(+) High LTV / Proceeds (though not as high as Fannie)

(+) Widespread availability (via authorized lenders in the OptiGo network)

CONS:

(-) Stringent eligibility criteria for property type and characteristics

(-) Poor prepayment flexibility (yield maintenance can be brutal)

(-) Time-consuming application process (could take months)

(-) Fairly strict borrower requirements

The agencies offer some of the best options for residential investors and will be a go-to provider for many as a result. Their fair borrower requirements, low rates, great terms, and non-recourse nature are ideal for newer and experienced investors alike.

Debt Provider #2 – The Banks:

The banks category includes three main tiers of banks: community, regional, and national. Community banks are the small ones who lend in their backyard. Regional banks often cover multiple states and may even be a division of a national bank. National banks are the behemoths like Chase, Wells Fargo, and Bank of America who have hundreds of thousands of employees and a worldwide presence.

You can generally categorize the loans that come from the banks into two categories: balance sheet loans and secondary market loans. Balance sheet, also known as portfolio loans, simply means the bank is keeping it on their own books. Secondary market loans are those that will be sold to someone else, often Fannie, Freddie, or to a CMBS provider in the manner discussed previously. If a lender is planning to hold the loan on their books, they can be much more nimble and flexible than in the secondary market since they have very box-like requirements that must be met.

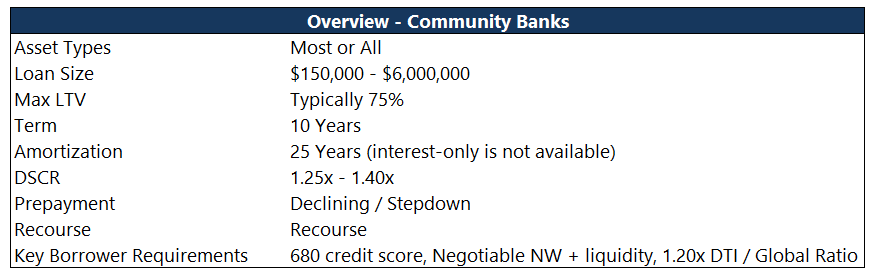

Community Banks – these are smaller banking organizations that operate in a local geography and do not have a regional or national presence. These banks typically emphasize a personal touch and will strictly “invest in what they know” (aka the immediate area that the bank operates in). Some examples I can think of include Lakeland Bank in New Jersey and Umpqua Bank in the Pacific Northwest. Unfortunately, it is inevitable that these will become absorbed by larger firms and may end up mostly extinct.

PROS:

(+) Personalized touch / relationship lending

(+) Nimble review and approval processes

(+) Emphasis on income, not net worth

(+) Fairly attractive leverage

CONS:

(-) Smaller loans

(-) Generally higher interest rates

(-) Limited geographic reach

(-) Interest-only is rare and amortization is stricter

(-) Recourse

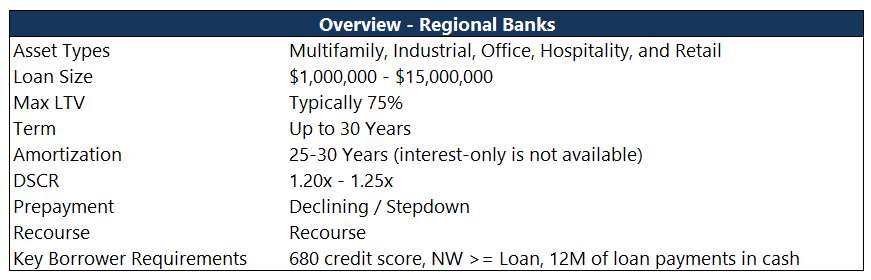

Regional Banks – these are the larger versions of community banks that typically operate in the major cities of a state or in a fairly standardized geographical definition such as the Northeast or Midwest. This subset received quite a bit of notoriety in 2023 when several of them suffered major liquidity and solvency issues, causing a nationwide financial panic. Several of them, including First Republic Bank and Silicon Valley Bank, failed. Well known “survivors” include Truist, Bank of the Ozarks, Fifth Third, and PacWest. Think of these groups like community banks with a slightly larger reach and whose ATMs you might find in more than 3 locations. This fiasco caused some apprehension in the real estate market because some studies say these regionals lend ~80% of all commercial loans which is astounding!

PROS:

(+) Excellent interest rates

(+) Personalized touch / relationship lending

(+) Local knowledge

(+) Strong array of product offerings

(+) Fairly attractive leverage

CONS:

(-) Smaller loans

(-) Stricter borrower requirements

(-) Interest-only is rare

(-) Recourse

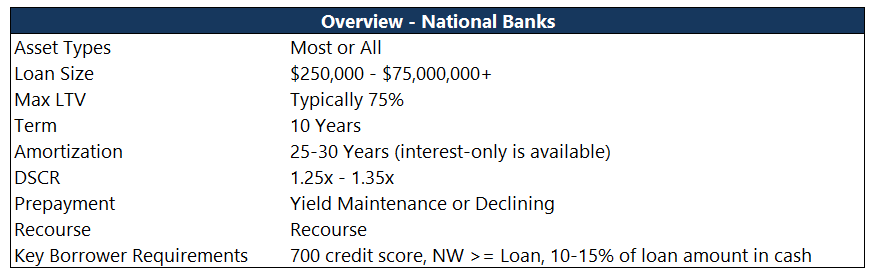

National Banks – these are the groups that top the list of largest banks by size in the states. The top 4 as of mid-2023 are JPMorgan Chase, Bank of America, CitiGroup, and Wells Fargo. These are gigantic conglomerates and have higher net worth, liquidity, income, and experience thresholds. These banks naturally have a lot of money to lend and can therefore get very competitive, especially if they fancy you (aka you are a major deposit-holder) and your deal.

PROS:

(+) Potentially the best interest rates

(+) Larger loans

(+) Massive array of product offerings

(+) Fairly attractive leverage

CONS:

(-) Stricter borrower requirements

(-) Interest-only is rare

(-) Lower loan duration

(-) Recourse

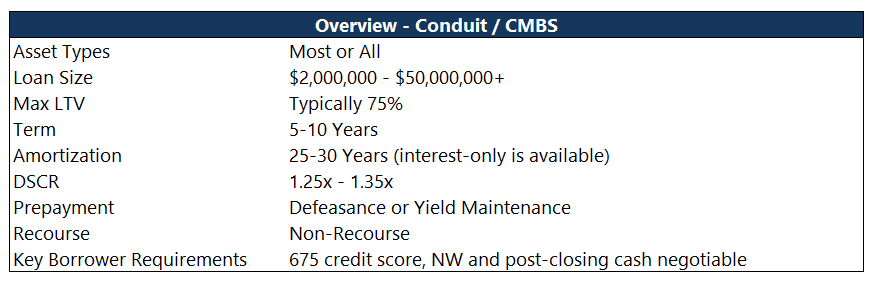

Debt Provider #3 – The Conduits:

Conduit is just a fancy encompassing word for CMBS and other “structured” products. Similar to the agencies, a conduit lender will close on a loan with their own money with the specific objective of securitizing them and selling them to investors on the secondary market. These are often structured into “tranches” of different risk / return levels. It could be from a single borrower or many different borrowers. For example, let’s say a conduit lender is going to group 10 loans totaling $100mm together at a weighted average interest rate of 5%. This does not mean they have to pick one investor who wants a 5% coupon to sell it to. They can break it up into 2 equal tranches of 8.0% (higher risk / higher return) and 2.0% (lower risk / lower return). They could break it up into 3 equal tranches of 7.0%, 5.0%, and 2.5% etc. There are all sorts of ways to cut it up including by maturity. Believe it not, most CMBS’ have 50-100 distinct loans in them!

Due to the combination of different loans of income-producing properties, these are often viewed as less risky and can provide attractive interest rates. It is also one of the most desirable securities on the secondary market catering to everyone from pension funds to hedge funds. For this reason, it is very liquid, which reinforces its ability to offer great rates.

PROS:

(+) Competitive interest rates (often lower than the banks)

(+) Lower credit requirements

(+) High LTV / Proceeds

(+) Assumable

(+) Non-Recourse

CONS:

(-) Not prepayable without penalty

(-) Standardized / inflexible terms

(-) Time-consuming application process

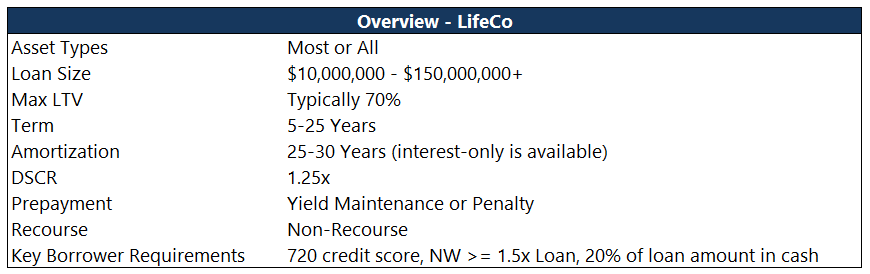

Debt Provider #4 – The Life Companies:

Most life insurance firms such as New York Life and MetLife are major providers of debt (and equity for that matter) capital in the real estate sector. Investing in real estate makes a lot of sense for them because their business model fits perfectly with the type of investor that real estate investments need. Remember, the entire LifeCo industry is just a spread business. They want to earn more in premiums than they have to pay out in insurance claims. Death is one of life’s few certainties and therefore they are able to project with reasonable accuracy when and what their outflows will be. The rest of their time can then be spent trying to maximize their inflows by investing the premiums they receive for the highest possible return given their allowable risk. LifeCo’s prefer long investment horizons, lower volatility, and desirable but stable yields, all of which can be provided by quality real estate. To protect themselves, they generally offer lower leverage and really emphasize the quality of the borrower, geography, and asset.

PROS:

(+) Excellent interest rates

(+) Larger loans

(+) Long duration

(+) Relationship lending

(+) Non-recourse

CONS:

(-) Strict borrower requirements

(-) Strict geography / asset criteria

(-) Lower leverage

(-) Lower flexibility

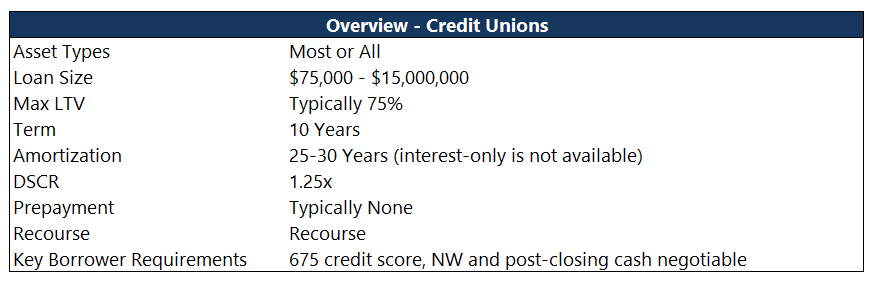

Debt Provider #5 – The Credit Unions:

Credit unions are organizations that are owned by their members and typically only offer services to other members. They are also different than the rest of the debt providers on this list in that they are not-for-profit and will never sell your loan. Credit unions exist solely to benefit their members. In certain situations, credit unions can be a real solid choice, such as if you would like zero prepayment penalties.

PROS:

(+) Competitive interest rates

(+) Personalized touch / relationship lending

(+) No prepayment penalty

(+) Approval / underwriting flexibility

CONS:

(-) Recourse

(-) Borrower must join the credit union

(-) Limited lending geography

(-) Fewer product offerings

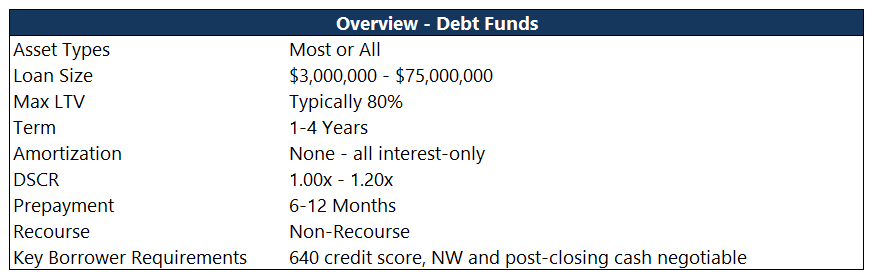

Debt Provider #6 – The Debt Funds:

Debt funds are usually divisions of private investment firms or PE shops who provide financing to a range of asset types and situations in commercial real estate. While they are often known simply for being more expensive, they are playing an increasingly important role in providing credit in the real estate and general investment community, especially as banks tighten up their belts. They can provide first mortgages, construction / bridge loans, and mezzanine / subordinated positions.

While debt funds will probably not be the first call you make when seeking out financing, these groups will find a way to lend on a truly compelling deal, as these are “business people” who have a better ability to understand a deal’s investment profile than a more check-the-box bank officer. This also allows them to work with you both during the underwriting process and throughout the investment period, and their experience and insights are a real asset to the borrower.

PROS:

(+) Flexible, common sense process

(+) Savvy businessfolks who can be an asset to the borrower

(+) Lower coverage requirements (if there is a clear path to value-creation)

(+) Higher leverage

(+) Many ways to structure

CONS:

(-) More expensive pricing and fees

(-) Shorter duration

(-) Stringent control and “covenants”

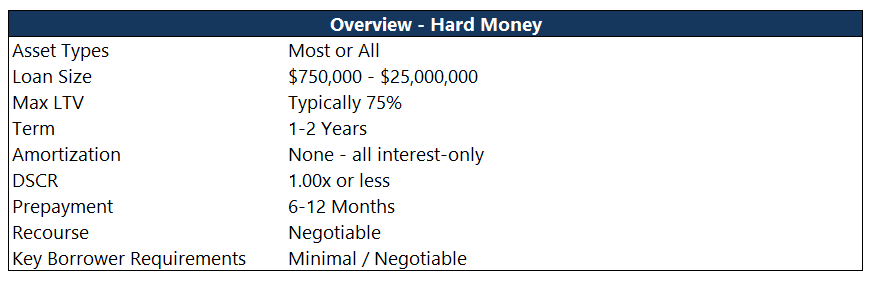

Debt Provider #7 – Hard Money:

Last on this list and hopefully last on a borrower’s call list are the hard money lenders. While there are of course benevolent shops, this group mostly consists of the industry’s “loan sharks”. They will look over your less than optimal liquidity and net worth while moving very quickly to get you approved. In exchange for this, they get to charge eye-watering rates and high fees.

PROS:

(+) Quick approval process

(+) Minimal borrower requirements / focus is on the asset

(+) Low coverage requirements

(+) Flexibility on structure

CONS:

(-) Very expensive pricing and fees

(-) Very short duration

(-) Unscrupulous players exist in the space

Bonus Debt Providers:

Some other debt sources that are out there are listed below. I did not include them in the main list because they are either too niche or I have not had enough experience with them to talk about intelligently:

Ginnie Mae – similar family and function as Fannie and Freddie except that it is fully owned by the federal government. Deals exclusively in government programs such as FHA, VA, and USDA loans.

Crowdfunding – a subset of private lending that raises money from “retail” investors to lend on projects the crowdfunder approves. They can move fast but are often expensive with potentially funky terms.

HUD – another government program that offers great rates and ultra long terms in exchange for nightmarish red tape and processes.

SBA – tailored for small businesses who have or want owner-occupied real estate. If you meet the eligibility requirements, this can be a great option for business owners.

Summary:

Debt financing is a key part in real estate investing and there are a ton of options out there to help you reach your objectives. Make sure you have a baseline understanding of all these main options so that you can make prudent financing decisions. In addition to your own knowledge, find a talented mortgage broker to work with on a regular basis.

Sources: Terry Painter, Apartment Loan Store, Janus, Walker & Dunlop, Eastdil