The Skinny:

Replacement cost is how much time and money it takes to build new buildings and should play a central role in your market and investment selection, as it is the main determinant of new competition.

What is Replacement Cost?

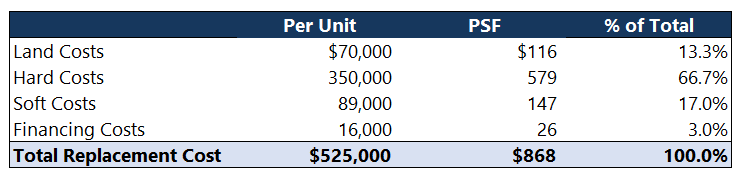

Replacement cost is simply what it costs to buy the land, entitle, and construct a new building that has the same aesthetics and functionality as an existing one. Every single building has a replacement cost and they can vary widely due to factors such as building type, location, and age (e.g. depreciated replacement cost). Shiny downtown towers have very high replacement costs while suburban self-storage facilities are very cheap. The three main components of replacement cost are materials, labor, and overhead / profit. The costs of each component have risen at or above inflation (3-4% / year) over the past two decades. Here is what a typical replacement cost budget would look like for an apartment building. This would essentially be a developer’s summarized budget. Note that replacement costs for residential are usually summarized on a “per unit” basis while office / retail / industrial use PSF.

The concept is fairly pervasive in real estate and is an especially important metric for insurance companies, who use it to determine the appropriate coverage. For example, if your property is worth $5mm (the price the market would be willing to pay) but the replacement cost is only $3mm, your coverage would be for the $3mm not the $5mm because the insurer does not care about the market value. A fun comparable would be a piece of gold. Let’s say you have a 1oz piece of gold directly from Blackbeard’s personal stash, which is incredibly rare and at a Sotheby’s auction would fetch $1mm. It’s replacement cost is just the 1oz gold spot rate (which as of the time of this writing is ~$2,000) because other than its goodwill and emotional value, it is still a commodity 1oz piece of gold.

Replacement cost is also a bit controversial with regards to its role in property analysis. Some say it is pretty much useless, while others might buy a property solely based on it. I must admit that I am a former hater of its usefulness. I firmly believed that a property should be valued independently of its replacement cost and instead be based on its merits as a cash-flowing investment. I thought why should I care what is cost if I can comfortably enjoy its economic benefits? While some of this thinking is valid, it is too provincial and misses many big picture issues. Replacement cost needs to be front and center when reviewing any real estate opportunity.

Why is Replacement Cost Important?

One of the biggest risks, if not the biggest risk, in real estate investment is competition. On a deserted island, if you are the only merchant who can provide water and bananas, you are the king. But if 100 other merchants join in and do the same, your business will be in trouble.

At its core, real estate is simply an ongoing battle between supply and demand. You want to be in areas with steady and growing demand but with built-in constraints to new supply. The vaunted “supply-demand imbalance” is a common refrain in pitch decks. While this may be a blunt way of putting it, it is true that most of the real estate industry’s objectives are to make employer and housing costs more expensive through rent increases (so it is understandable why real estate investors often get a lot of flak). The most surefire way to accomplish this is to have demand outpace supply. If more and more people are competing to buy your limited amounts of water and bananas, you can charge more for them, simple as that.

Since I am enjoying this deserted island metaphor, I will keep it going. Replacement cost is the primary gating issue to new supply. It represents the cost to set up new water and banana stands. Costs could mean literal “hard” costs, such as the materials required to build the stand or “soft” costs such as the permitting and approval process that actually allows you to build and operate the stand. If hard costs are very expensive or if the permitting process is a total nightmare, new merchants would be discouraged from building new stands because both the return on investment (ROI) and return on hassle (ROH) are simply not worth it. Like any rational businessperson, real estate investors will not undertake any projects if there is not a reasonable rate of return.

In many major gateway cities, getting approvals to build new real estate is oftentimes tough. Construction costs and timelines are continually making it harder for new builds to “pencil”. The approval time alone could be 2+ years and the actual construction timing could take another 2+ years. A lot can change in 4-5 years, so it is an inherently risky venture that not everyone has an interest in taking on.

The crux of replacement cost is this: if a developer can build for $X and sell for $X + an attractive profit margin, they will build. If they cannot, then they will not build. Why on earth would a developer take on all the risks and headaches to build units at $500k, that would only sell for $400k in the open market? Locking in an immediate guaranteed loss of 20% is not exactly elite business sense. There are plenty of cities where the market price is lower than the replacement cost, and those are the places that will not see any new supply unless the developers have a desire to go bankrupt.

Find the markets where it is difficult for new water and banana stands to be built. More competition is the enemy. As the late and great Sam Zell said:

“There’s no substitute for limited competition. You can be a genius, but if there’s a lot of competition, it won’t matter. I’ve spent my career trying to avoid its destructive consequences.”

Focus on cost, geographical, and governmental constraints. If you are able to get a good portfolio of water and banana stands with a limited risk of new entrants, you are guaranteed to do well for yourself as you will be a provider of one of the most non-discretionary expenses in life.

Is it a Sin to Buy Above Replacement Cost?

I often ask this question to peers in my industry, and some are adamant that they would never buy a property for above replacement cost. While of course it is more desirable to buy deals below replacement cost, it is not a sin and there are several instances where it may make sense to do so.

The most prominent instance I can think of is if it is really good real estate in a market where new supply is very rare. Take a prime apartment tower in San Francisco. Whatever your view on the city, it is objectively one of the most supply constrained housing markets in the world. Even if it costs $1mm / door to build, it might make sense to pay 20%+ more than that to acquire it. Why? Well because the fundamentals are THAT good. Despite constant bets against SF, supply is so limited that owning a piece of good real estate can provide you with a great return even if you feel like you are overpaying in the beginning.

Another instance where paying above replacement cost would not be an issue is if you plan to hold for the very long term and are comfortable with the underwriting and market dynamics. Obviously you do not want to overpay in a place where inventory is going to double, but if you like your cap rate and do not need much rent growth to meet your financial goals, you will pay the strike price and just “clip coupons” for the long term. This is the MO for many “core” investors.

The truth is that people and investors buy above replacement cost all the time. After all, the homebuilding and apartment “merchant” building industries would not exist if no one bought properties above replacement cost. It is a cycle. When the market price < replacement cost, new supply stagnates while demand continues upwards, which in turn puts price pressure on the existing supply, which in turn makes the market price > replacement cost, which in turn makes it profitable to build again, which in turn increases the supply and so on and so forth. It is not a sin to participate in this cycle. It all depends on your investment objectives and horizon. However, choosing markets where you can buy good real estate at below replacement cost insulates you from this cycle because you know that new supply will not threaten you, and this allows you to sleep better at night.

Summary:

Replacement cost is a vital concept in real estate. It is the main determinant of the current and future likelihood of new supply, which is one of the biggest risks to a real estate investor. You must have a firm grasp on the replacement cost in your market. Unless there are specific circumstances that permit it, always seek to buy at an all-in basis that is meaningfully below replacement cost as it is the best natural hedge against new competition.